WARNING: Unknown Impersonators Target Correct Capital Wealth Management and CEO Brian I. Pultman on WhatsApp

Multiple Employer Plans: How They Work, and Would One Work for Your Business?

Multiple Employer Plans: How They Work and Would One Work for Your Business? The benefits of offering a retirement plan for businesses of any size are well-documented. Employees love it, as do business owners. Still, administrative burdens, high fees, and liability concerns keep many employers from being able to offer a plan with the full benefits they want. Multiple employer plans (MEPs) are specifically designed to eliminate the most significant barriers to entry.

Correct Capital Wealth Management is an independent financial advisory firm with over 80 years of combined experience that operates retirement plans for businesses and participants around the country. Keep reading to learn more about MEPs and how they could help your business, give us a call at 877-930-4015, or contact us online to speak to a financial adviser about your company's needs today.

What is a Multiple Employer Plan (MEP)?

A multiple employer plan is a type of IRS-approved, tax-advantaged, employer-sponsored retirement plan wherein multiple, unrelated employers come together into a single plan to achieve economies of scale. MEPs are organized and run by "MEP sponsors," who handle administrative duties and take on a portion of the fiduciary liability. MEPs can be either defined-benefit (pension) plans or defined-contribution plans; most are set up as 401(k)s.

There are two main reasons for employers to enter MEP:

- Achieve better per-participant costs

- Streamline and reduce management and compliance loads by placing the plan in the care of professional retirement consultants

MEPs originated with the 1947 Taft-Hartley Act, and were originally intended to allow collectively bargained or union workers in the same industry to pool their resources for retirement planning. MEPs have since evolved to largely involve employers in the same industry, i.e. construction companies and contractors, who are unrelated for tax purposes.

There are generally four entities involved in an MEP:

- An MEP Sponsor, such as an association, which offers the retirement plan to members.

- An adopting employer (your business), who offers the plan to their employees and processes contributions.

- A record keeper, that:

- Acts as custodian of plan assets

- Tracks eligibility and contributions

- Handles distributions

- Provides customer service, account statements, and online client portals

- An ERISA 3(38) financial advisor (such as Correct Capital), who works closely with the other parties to monitor and maintain plan investments and offer employee education and individual advice to employees.

How Are Multiple Employer Plans Different from Single-Employer Plans?

The main functional difference between MEPs and single-employer plans like 401(k)s is who is responsible for administration and investment. In a single-employer plan, day-to-day management, compliance, and other duties are retained by the employer. In an MEP, many of those responsibilities are shifted to the independent fiduciaries that take on many responsibilities typically handled by a single employer or plan sponsor. In an MEP, the MEP sponsor:

- Assumes day-to-day administrative duties

- Is responsible for hiring and monitoring service providers

- Oversees investments and funds management

- Assumes compliance responsibilities, etc...

What responsibilities are left for the employer/adopter? Just two:

- Sign the adopter/plan provisions agreement

- Provide contributions and employee census data

In return for having reduced responsibility, plan members also lose control over some important decisions that they would otherwise have complete control over. However, experienced fiduciary advisors who put your and your employees' interests above all can assure you that your plan participants and beneficiaries are in good hands.

Three Types of Multiple Employer Plans

MEPS are typically set up in one of three ways:

- Closed MEPs are made up of multiple, unrelated employers that are part of a "bona fide" group or association. "Bona fide" means the employers share a commonality beyond their 401(k), such as being in the same industry or if sharing common affiliation or ownership.

- Association retirement plans are a sort of "soft" closed MEP or "half-open" MEP. Employers in different industries in the same geographic region can join, as can employers in the same industry in different regions, as well as self-employed working owners.

- Pooled employer plans, or PEPs, are a newer type of plan introduced with the SECURE Act. PEPs function similarly to MEPs, except that employers are not required to have a common link such as geography or industry. PEPs must be sponsored by a "Pooled Plan Provider," registered with the DOL and IRS to act as fiduciary.

Most MEPs are closed MEPs. A financial advisor can help you determine which type of MEP may be best for your business.

Benefits of a Multiple Employer Plan

What do companies get out of joining an MEP? A wealth of advantages:

- Lower fees through economies of scale

- Retain enough flexibility for customized plan designs, i.e. – the adopting employer decides what's best suited as na discretionary employer contribution, via a matching rate or profit sharing formula

- Spread risk and transfer liability to experienced fiduciaries

- Reduced or eliminated administrative burden on your staff

- Eliminate retirement plan audit cost typically paid by the company/plan sponsor

- Payroll integration with many payroll companies

- Access to best-in-class investments and risk-based asset allocation models

- The knowledge, insight, and guiding hand of fiduciary financial advisors and CERTIFIED FINANCIAL PLANNER™ professionals

- Attract, retain, and motivate a skilled workforce by offering a robust retirement plan

Would a Multiple Employer Plan Work for My Business?

An MEP might be a good fit for you if your business falls into any of the following categories:

- Start-ups and small businesses — For smaller companies looking to offer their first retirement plan, MEPs provide a cost-effective solution and access to plans with greater benefits.

- Employers looking for a more robust plan — Small businesses who have "outgrown" their IRA-based SIMPLE-IRA or Simplified Employer Plan (SEP) are provided an easy way to upgrade into a robust 401k via an MEP, without the burdens and time consuming work of starting up a single employer plan on their own.

- Employers tired of high-fee plans — Companies frustrated with excessive fees from their current retirement plans might find MEPs a more economical alternative, offering better value and potentially enhanced services due to economies of scale.

- Employers needing fiduciary support — Firms concerned about fulfilling fiduciary responsibilities or lacking in-house expertise can benefit from the shared fiduciary roles in MEPs, ensuring compliance and informed decision-making.

- Employers looking to relieve administrative burdens — Companies wanting to reduce the time and resources dedicated to plan administration will find MEPs appealing, as the bulk of these tasks are managed by the MEP sponsor.

- Businesses with a diverse workforce — Companies, especially in industries like construction, architecture, and contracting, with varied employee roles and needs, can leverage the flexibility of MEPs to offer tailored benefits that cater to everyone.

- Companies aiming to enhance employee retention — Businesses looking to improve their benefits package to attract and keep top talent might find MEPs an effective strategy, given the comprehensive and often higher-value retirement solutions they can provide.

MEPs are often great retirement plans for the construction industry, and make sense in a variety of industries including retail, manufacturing, trucking, entertainment, and more.

Factors to Keep in Mind When Considering a Multiple Employer Plan

Some things to look at to see if your business is a good fit include:

- Company size — While MEPs can be beneficial for small to medium-sized businesses due to shared costs and responsibilities, larger companies might find that they can negotiate similar benefits and costs on their own, or may want more control over plan specifics.

- Current retirement plan status — If your company already has a retirement plan in place, consider the costs and benefits of transitioning to an MEP versus enhancing your existing plan.

- Administrative capabilities — Evaluate your internal resources. If your business lacks the expertise or capability to administer a retirement plan, an MEP's shared administrative structure might be advantageous.

- Long-term business goals — Align your retirement benefits strategy with your broader business objectives. If growth, mergers, or acquisitions are on the horizon, consider how an MEP might fit into these plans.

Get Started With Your Multiple Employer Plan Today

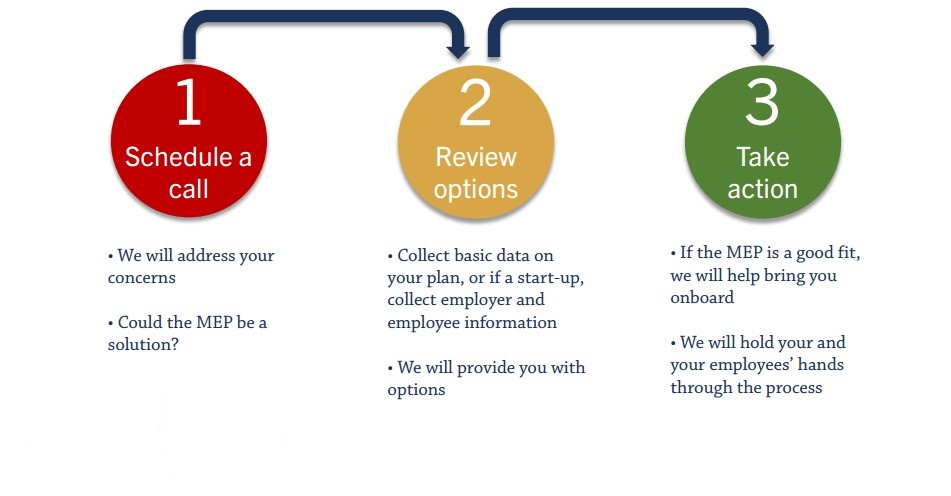

Correct Capital is an ERISA 3(38) advisory firm in St. Louis, MO that specializes in small business retirement plans and MEPs. If you think an MEP is a good fit for your business, our process to get started consists of three easy steps:

From cost savings to administrative ease, and from fiduciary support to employee satisfaction, MEPs are a great retirement plan solution for many small- and medium-sized businesses. Reach out to Correct Capital today for a personalized consultation. Schedule an appointment with a member of our advisor team, call us at 877-930-4015, or contact us online to get started.

Correct Capital

Wealth Management

130 S Bemiston Ave,

Suite 602

Clayton, MO 63105

+1 (877) 930-4015

View on Google Maps

Services We Offer

- Retirement Planning Services

- Financial Advice

- 401(k) Rollover

- Financial Portfolio Management

- Retirement Consultant

- Asset Management

- Financial Advisor

- 401k Companies

- Wealth Management

- Rollover 401(k)

- Retirement Planning

- Retirement Calculator

- Social Security Consultants Near Me

- Tax Planning

- Small Business Retirement Plans

- 401(k) For Small Business

- Self-Employed Retirement Plans

- ESOP Advisor

- Company 401(k) Plans

- Fiduciary Financial Advisor

- Succession Planning

- Retirement Plan Consultants

- Financial Planning

- Retirement Planner

- High-Net-Worth Wealth Management

- 401(k) Audit

- Investment Management

- Roth Conversion

- Independent Financial Advisor

- Retirement Financial Planning

- Investment Planning

- Retirement Income Planning

- Comprehensive Financial Planning

- Financial Planning for Business Owners

- Family Wealth Planning

The opinions expressed in this program are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security. It is only intended to provide education about the financial industry. To determine which investments may be appropriate for you, consult your financial advisor prior to investing. As always please remember investing involves risk and possible loss of principal capital; please seek advice from a licensed professional.

Correct Capital Wealth Management is a registered investment adviser. Advisory services are only offered to clients or prospective clients where Correct Capital Wealth Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Correct Capital Wealth Management unless a client service agreement is in place.