WARNING: Unknown Impersonators Target Correct Capital Wealth Management and CEO Brian I. Pultman on WhatsApp

Retirement Spending Behaviors That May Surprise You

Effective retirement planning requires a disciplined approach to ensure your money is grown, spent, and saved in accordance with your goals. But disciplined doesn’t mean rigid. In uncertain times smart retirees need to modify their spending behavior to ensure their financial situation stays stable.

In this episode of Capital Conversations, hosts John Biedenstein and Steve Paulus share some new research and explore how retirees should approach the classic 4% withdrawal rule and their income planning given the current market declines.

For recent investment news and our take on the current market,retirement planning, and investment, listen to our podcast Capital Conversations or view our recent blog posts.

Below is the transcript of our most recent episode of Capital Conversations, "Retirement Spending Behaviors That May Surprise You."

John Biedenstein: Welcome back for another session of Capital Conversations. My name is John Biedenstein.

Steve Paulus: And I'm Steve Paulus.

John Biedenstein: We want to go over today some information that might surprise you, but we think it's pertinent to bring to [your attention]. It's actually some information regarding spending behaviors in retirement.

Steve Paulus: That's right, John.

One of the things that has always been talked about is the classic 4% withdrawal rule. And one of the things that I think we've come across that's interesting is that, that 4% withdrawal, it’s always assumed that it's constant. No matter what happens in the economy, no matter what happens in your portfolio, that 4% stays constant.

And what we found in some new research that's come up is that, as you know, that's not true. People actually modify their spending behavior in retirement. And I think that's a really important point to consider, John.

John Biedenstein: Especially in the market activity that we've seen lately, where you have market declines. And what we've seen is a lot of our clients and a lot of retirement plan participants become frugal. They tend to spend less during retirement.

T. Rowe Price provided a recent survey which indicated that one third of retirees, 20 years after they started retirement, their retirement plan balance is approximately the same. And at death, again with about a third of those folks, the balance was the same. So, what we have seen is people do spend less when the market declines. Only 8% would use their retirement savings to maintain their spending. So, a greater majority are actually spending less.

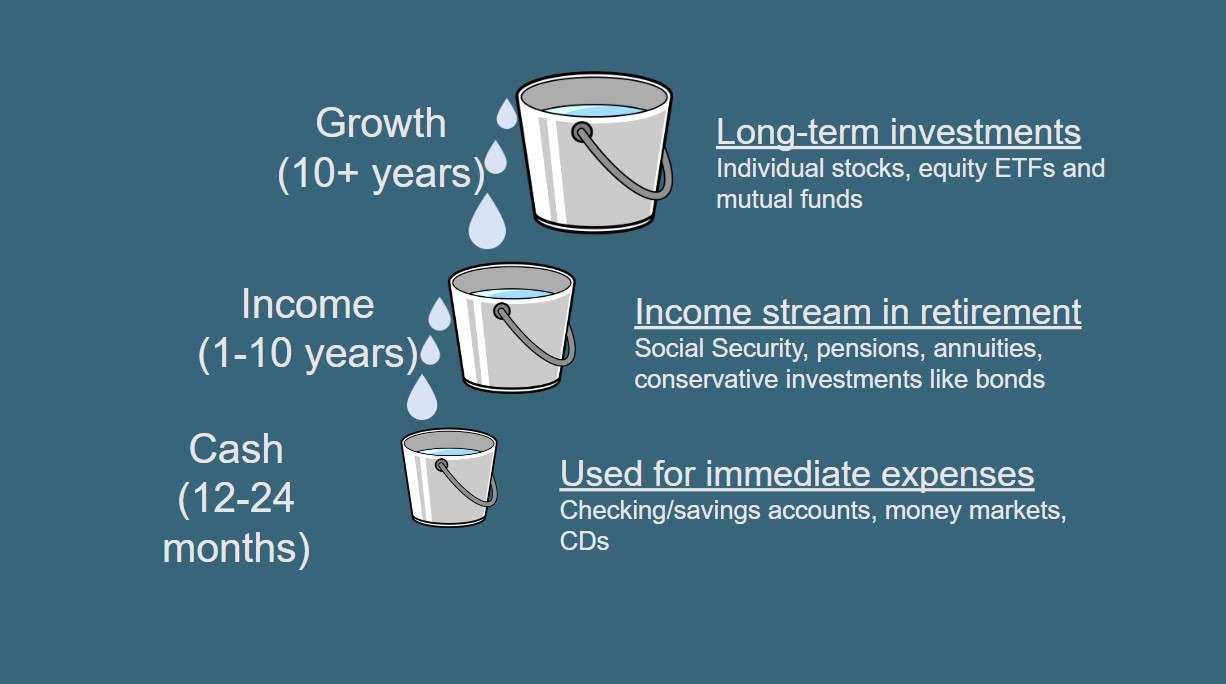

What I really think it complements is the retirement strategy that we've talked about where you have buckets of money that people have during retirement and you always have a “growth bucket.” For five or ten years out as you get older, you always have a bucket of money that you're looking to get the most out of. And you've got cash reserves, you've got money that you have readily accessible. So folks that are doing that tend to not have to pull money out of [their] investment accounts during market declines. So, again, it's positive information that we've seen that all of the things that we talk about, clients actually do.

Steve Paulus: Exactly. And I think one of the things that was also important in those numbers you gave, John, is that that was for a portfolio of $500,000 or less. It wasn't somebody who had two or three million dollars in net worth. So you think, “Well, yeah, of course you can modify your spending if you have that much.” In reality, you're talking about people who have a starting balance of $500,000 or less, and their non-housing wealth 20 years after [they] retire is the same, or 68% – more than half of their non-housing wealth – had increased, which again speaks to the point of we all do the same thing. If something becomes more expensive, we pair back in another area because we know we want to keep that principle, that corpus of what we've accumulated, safe and secure. Because we don't know what's going to happen 20 years down the road. We don't know what health care we're going to have. We don't know what other demands on our money we're going to need to account for.

So I think it's an important point that when you hear that 4% withdrawal rate, you can take that with a grain of salt. That's not a constant rate. When things are flush and things are going well, you can spend a little bit more. When they're not going as well, you can still maintain a great lifestyle just by pulling back on some of the things that aren't as much of a necessity.

John Biedenstein: Yeah. The last thing I'll say is, folks that are newer to retirement, you might be spending more in your first year in retirement. But again, you have to put your long-term hat on to think that two or three years down the road, you want to look back at this and say, “Did I take my withdrawals at the right time?” And candidly, what we're seeing is most people are doing that.

Steve Paulus: That's right. And you know, what we do here at Correct Capital is we have the kind of the three buckets, I call them. You have your income, your cash, which you're going to use right now or the next couple of years. Then you have your income bucket, which you're going to use beyond that. And then you have the growth bucket, when the cash kind of gets paired down, you pull from income, and when income gets pulled down, you pull from your growth side. So that way we see that that's one of the means by which people do modify what they spend, depending on what the bigger macro environment is.

Disclaimer: The opinions expressed in this program are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security. It is only intended to provide education about the financial industry. To determine which investments may be appropriate for you, consult your financial advisor prior to investing. As always, please remember, investing involves risk and possible loss of principal capital; please seek advice from a licensed professional.

Correct Capital Wealth Management is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Correct Capital Wealth Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Correct Capital Wealth Management unless a client service agreement is in place.

Capital Conversations by Correct Capital Wealth Management

Understanding the dynamics of retirement spending and maintaining flexibility is crucial for financial well-being and long-term security. If you have questions or need personalized advice to navigate your own retirement journey, reach out to a financial advisor from Correct Capital Wealth Management at 3877-930-4015 or contact us online.

Correct Capital

Wealth Management

130 S Bemiston Ave,

Suite 602

Clayton, MO 63105

+1 (877) 930-4015

View on Google Maps

Services We Offer

- Retirement Planning Services

- Financial Advice

- 401(k) Rollover

- Financial Portfolio Management

- Retirement Consultant

- Asset Management

- Financial Advisor

- 401k Companies

- Wealth Management

- Rollover 401(k)

- Retirement Planning

- Retirement Calculator

- Social Security Consultants Near Me

- Tax Planning

- Small Business Retirement Plans

- 401(k) For Small Business

- Self-Employed Retirement Plans

- ESOP Advisor

- Company 401(k) Plans

- Fiduciary Financial Advisor

- Succession Planning

- Retirement Plan Consultants

- Financial Planning

- Retirement Planner

- High-Net-Worth Wealth Management

- 401(k) Audit

- Investment Management

- Roth Conversion

- Independent Financial Advisor

- Retirement Financial Planning

- Investment Planning

- Retirement Income Planning

- Comprehensive Financial Planning

- Financial Planning for Business Owners

The opinions expressed in this program are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security. It is only intended to provide education about the financial industry. To determine which investments may be appropriate for you, consult your financial advisor prior to investing. As always please remember investing involves risk and possible loss of principal capital; please seek advice from a licensed professional.

Correct Capital Wealth Management is a registered investment adviser. Advisory services are only offered to clients or prospective clients where Correct Capital Wealth Management and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Correct Capital Wealth Management unless a client service agreement is in place.